SGX Monthly Newsletter

Monthly Newsletter

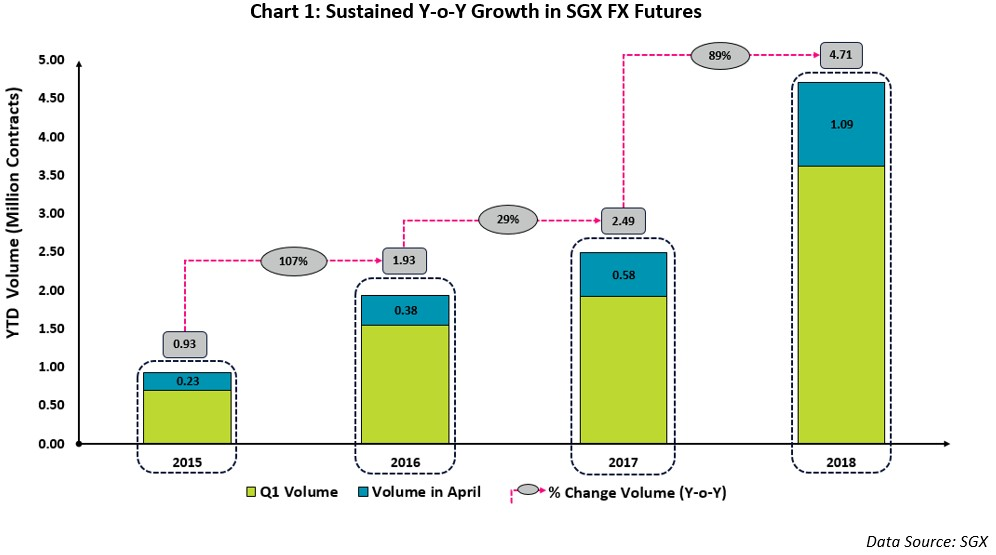

SGX FX Futures volume exceeds a million contracts for the fourth month in a row; YTD volume up 89% Y-o-Y

Cumulative volume since inception for SGX USD/CNH and INR/USD futures crossed US$ 1 trillion Aggregate YTD SGX FX futures volume in excess of 4.71 million contracts; y-o-y growth at 89% Highest single day volume for SGX USD/CNH futures of US$ 2.65 billion on 12 April

YTD SGX USD/CNH futures crossed US$ 115 billion; YTD volume growth at 207% y-o-y

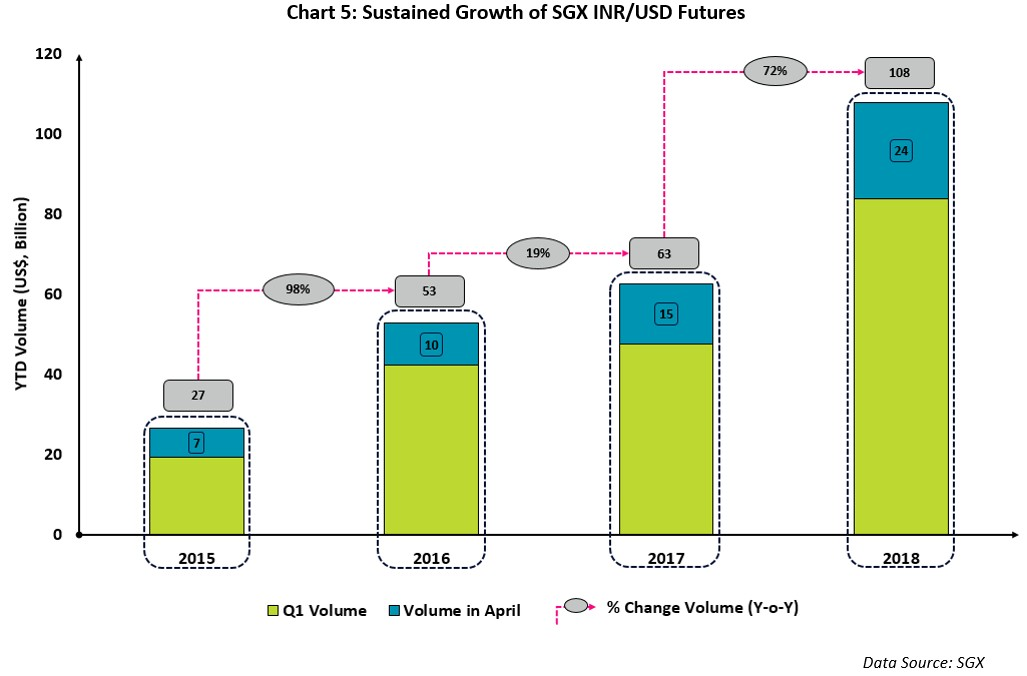

Rupee depreciated 2.7% in April hitting a 13-month low; SGX INR/USD futures YTD volume (notional terms) up 72% y-o-y

April was yet another month packed with headlines. Early in the month, the threat of a US-China trade war ratcheted up a notch when US announced more tariffs on Chinese goods including key sectors like IT, robotics and communication technology. With the move likely to hit the growing Chinese technology and telecom businesses, China responded by adding over 100 items imported from US, to its own list of tariffs mechanism.

However, a trade war was not the only risk that global markets had to manage in the month. Geopolitical risks entered the frame when the US and a few allies (UK, France) launched air strikes on Syria over suspected weapons attacks, further escalating tensions between the US and Russia. Ex-CIA director Mike Pompeo made a secret visit to North Korea to meet up with the leadership and subsequently took over as the new US Secretary of State upon his return. However, recently observed nuclear tensions in the region gave way to hopes of peace towards the end of the month. The North Korean leader crossed over the demilitarized border to meet with his South Korean counterpart in a historic event. Together they agreed to announce the end to the ongoing hostilities between the two nations. The South Korean Won that had weakened since end of March partially recovered after the news.

Global financial markets have started to feel the pressure of rising US yields and in April, the 10-year benchmark broke past 3% after four years. As a result, the yield differential with EM countries has started to narrow, potentially influencing fund flows and asset valuations. Oil importing emerging markets such as India have also been hit by the rise in crude oil prices and the Indian capital markets lost steam amidst inflationary fears and capital outflows. Even the renminbi depreciated against the dollar in April, bucking a trend that has continued for over a year.

SGX continues to be the venue of choice to manage market risk during periods of market turmoil, with the trading in FX futures exceeding a million contracts for the fourth month in a row. At nearly 1.09 million contracts traded in April (Chart 1), the volume for SGX FX futures was up by half a million contracts over April 2017. The cumulative open interest for all FX contracts is also up 37% m-o-m and 74% y-o-y. In April, SGX also crossed a significant milestone of US$ 1 trillion dollar worth of cumulative notional trading in INR/USD and USD/CNH futures since their inception.

SGX USD/CNH futures crossed US$ 115 billion in 2018; Renminbi weakened in April

It would have been natural to expect some volatility for the renminbi given the posturing on trade tariffs at the start of April. By the end of the month though, not much seemed to have changed.

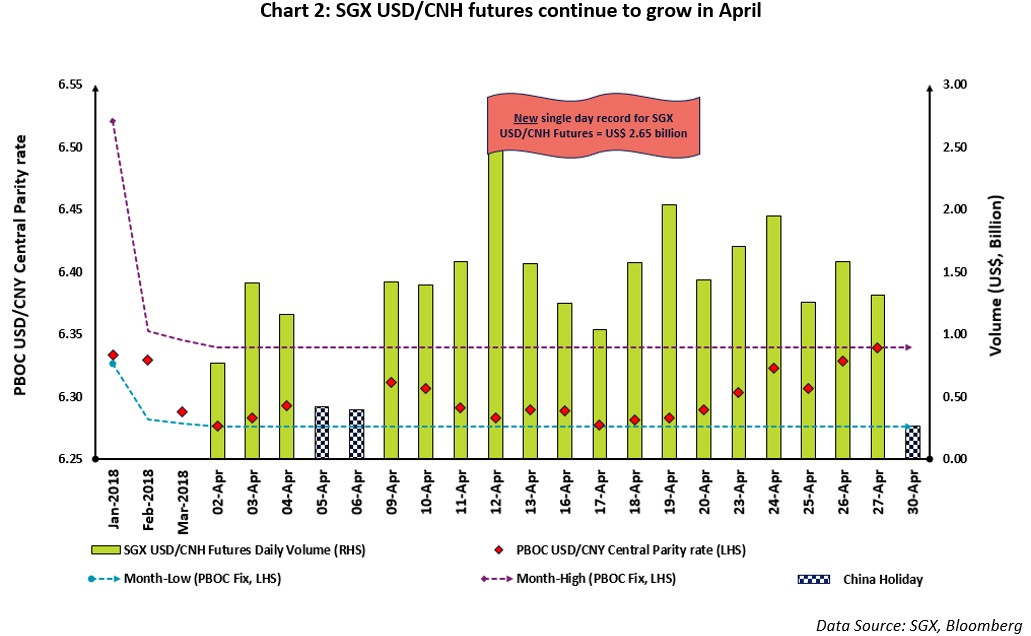

April began with three Chinese holidays in the first week. While that may have helped cushion the market impact of the trade war rhetoric, it also meant that the renminbi trading was off to a slow start. However, the second week saw trading get into higher gear as markets resumed after the break. On 12 April, the renminbi weakened slightly amidst reports that Beijing may be reviving outbound investment schemes after a three-year hiatus. This raised the likelihood of more capital outflows and proved to be the best day for SGX USD/CNH futures trading since their launch in 2014 (Chart 2). Driven by the global macro environment, the SGX USD/CNH futures traded a phenomenal US$ 2.65 billion on that day [26,539 contracts].

The shrinking yield differential between the US and China no longer seems to support the case for a stronger renminbi and the expectations of a weaker renminbi seem to be on a rise. Industrial profits data that suggested a weaker business environment and slower growth rate than the pace seen a year ago, also contributed to the slide in April and led some analysts to revise their forecasts. Short dated interest rates in HK usually spike because of the month-end effect as banks hold renminbi to meet liquidity requirements imposed by the central bank. With the peak period of corporate tax payments approaching, the funding has been tight in China and the overnight funding rates shot up. An extended holiday towards the end of month also weighed in as the overnight CNH Hibor rate jumped by 1.5 percentage points to 5.204% (TMA Fixing on 27 April). The move was the biggest gain since late November last year.

While both the US and China took turns to announce their own list of goods for tariffs, the renminbi continued

to stay range bound. The USD/CNY central parity rate set by PBOC continued to put the renminbi at levels not seen since mid - 2015 and the currency strengthened until 19 April, after which it changed direction, ending the month at 6.3393, or 0.8% weaker than the previous month close.

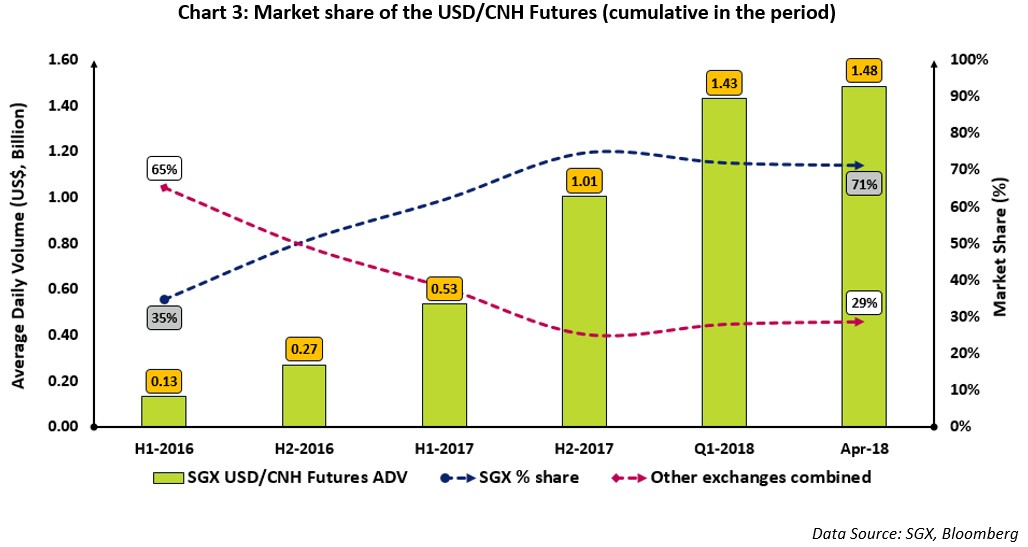

April was also the first time that the SGX USD/CNH futures traded in excess of US$ 1 billion for 15 successive days. This is the longest stretch of days with volume exceeding US$ 1 billion since the inception of contract in late 2014 and beat the previous run of 13 days that had ended a few weeks ago on 12 March. The Average Daily Volume (ADV) for the SGX USD/CNH futures contract has also continued to grow this year and closed in on US$ 1.5 billion in April (Chart 3), up from US$ 1.1 billion at the end of last year. SGX has already cleared over US$ 115 billion for the contract since the start of 2018, which represents an increase of 207% from the corresponding period in 2017. The YTD volume for the contract [1,155,550 contracts] has already reached 61% of the full year volume in 2017, underscoring a significant increase in SGX's role for market risk management. The weakening of the currency in April is a timely reminder that a continuous strengthening of the renminbi is no longer a foregone conclusion and that market forces will continue to play their part in determining its course. This raises the importance of venues that offer robust risk management solutions for international participants.

Rupee hit a 13-month low in April; YTD SGX INR/USD futures volume up by 72% y-o-y

![]() Indian bonds have recently been in decline amid excessive debt supply, concerns about inflation and higher global bond yields. The Indian regulators have taken several steps to remedy the situation and boost the domestic fixed income markets.

Indian bonds have recently been in decline amid excessive debt supply, concerns about inflation and higher global bond yields. The Indian regulators have taken several steps to remedy the situation and boost the domestic fixed income markets.

In late March, the Indian government announced a slowdown in the pace of borrowing that led to a flattening of the yield curve. April began in much the same way when RBI announced that Indian banks could spread out the mark to market (MTM) losses on bonds over four quarters in a bid to improve their loss absorption ability and to encourage them to continue buying sovereign bonds. On 9 April, India extended the quota for foreign investors to participate in the Indian government bonds allowing foreigners to own 6% of sovereign debt by 2020.

Expectedly, these measures provided a fillip to the market and the sovereign Indian bonds rallied in expectation of a sustained bull run in the bonds with these moves seen to deepen the participation of foreign institutions. However, the rally did not last long. The renewed fears of a widening current account deficit took hold and bonds lost most of the gains in a matter of days as bond yields retraced the levels prior to the announcement.

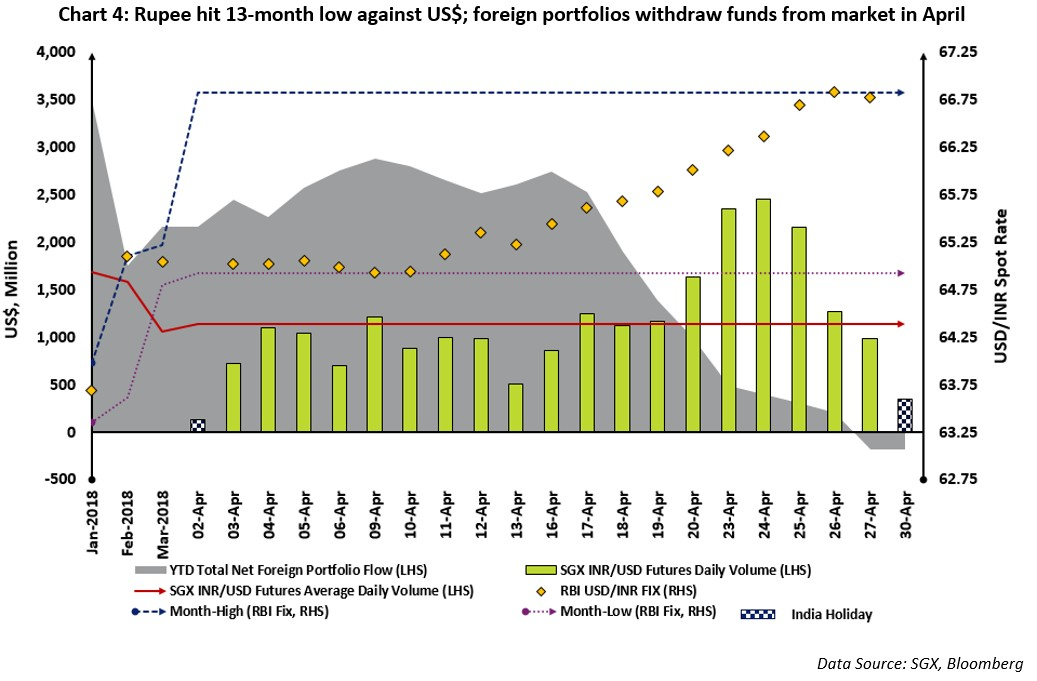

The portfolio flows from foreign institutions (FPI), ended the month as net negative for the year, wiping the gains made early in the year (Chart 4). With the foreign portfolios withdrawing funds in April, the rupee traded in a wider range than in March. The flow from foreign funds was net positive for the first two weeks, with the fixed income inflows providing cushion against the withdrawals in equity. Rupee weakened against the greenback every single day in the third week of the month as portfolio withdrawals grew larger and turned net negative for the month. Rupee eventually weakened to its lowest in more than a year and broke back above 66 against the dollar [RBI Fix: 66.0167] on 20 April as fears of a widening current account deficit took hold in April. The rupee continued to weaken through the second half of April and ended the month at 66.7801 [RBI Fix as on 27 April].

Also contributing to the slide was a hawkish outlook on interest rate from RBI. A revival in investment activity and an improvement in capacity utilisation has been good for economy and the RBI had decided to keep the rates stable in its last policy meeting while expecting the inflation to ease later in the year. However, the minutes of the Monetary Policy Committee meeting, released on 20 April, suggested a more hawkish tone, leading many market observers to believe that the RBI might soon ditch an accommodative policy and hike key rates.

After a strong start to the year, rupee trading drifted lower in March across all venues and it reflected in the

lower ADV for the SGX INR/USD futures for the month. April too had a slow start with muted activity in the first few days. However, the market turmoil in the third week of April made up for a slow start to the month and contributed to eight successive days of trading volume above US$ 1 billion for the SGX INR/USD futures. This included three consecutive days of trading over US$ 2 billion, second such instance in 2018.

In the run up to the elections next year, the Indian economy faces challenges in the form of increased government expenses and food subsidies to farmers look most likely to derail the government's budget in addition to the rising crude oil prices. Any reduction in capital inflows is likely to add to the economic stress. While the 10-year US dollar yields have slowly but surely crept up above the historically relevant 3 percent threshold, the yields on the benchmark 10-year Indian government bonds have continued to stay close to 8 percent. Rupee has already lost nearly 4.5 percent against the greenback this year and while the yield differential could yet bring investors back and boost the currency, many sell-side analysts have revised their forecasts on the rupee in expectation of further weakening.

The volume for the SGX INR/USD futures continues to grow steadily in 2018. Trading in SGX INR/USD contract has already crossed US$ 1 billion threshold 54 times in the current year (including 11 times in April) and compares well to the 19 such days for the corresponding period in 2017. At US$ 108 billion worth of notional trading, the YTD volume (notional terms) for SGX INR/USD futures in 2018 is up 72% y-o-y, bolstered by a robust US$ 24 billion show in April (Chart 5).

This document/material is not intended for distribution to, or for use by or to be acted on by any person or entity located in any

jurisdiction where such distribution, use or action would be contrary to applicable laws or regulations or would subject Singapore Exchange Limited ("SGX") to any registration or licensing requirement. This document/material is not an offer or solicitation to buy or sell, nor financial advice or recommendation for any investment product. This document/material is for general circulation only. It does not address the specific investment objectives, financial situation or particular needs of any person. Advice should be sought from a financial adviser regarding the suitability of any investment product before investing or adopting any investment strategies. Use of and/or reliance on this document is entirely at the reader's own risk. Further information on this investment product may be obtained from www.sgx.com. Investment products are subject to significant investment risks, including the possible loss of the principal amount invested. Past performance of investment products is not indicative of their future performance. Examples provided are for illustrative purposes only. While each of SGX and its affiliates (collectively, the "SGX Group Companies") have taken reasonable care to ensure the accuracy and completeness of the information provided, each of the SGX Group Companies disclaims any and all guarantees, representations and warranties, expressed or implied, in relation to this document and shall not be responsible or liable (whether under contract, tort (including negligence) or otherwise) for any loss or damage of any kind (whether direct, indirect or consequential losses or other economic loss of any kind, including without limitation loss of profit, loss of reputation and loss of opportunity) suffered or incurred by any person due to any omission, error, inaccuracy, incompleteness, or otherwise, any reliance on such information, or arising from and/or in connection with this document. The information in this document may have been obtained via third party sources and which have not been independently verified by any SGX Group Company. No SGX Group Company endorses or shall be liable for the content of information provided by third parties. The SGX Group Companies may deal in investment products in the usual course of their business, and may be on the opposite side of any trades. SGX is an exempt financial adviser under the Financial Advisers Act (Cap. 110) of Singapore. The information in this document is subject to change without notice. This document shall not be reproduced, republished, uploaded, linked, posted, transmitted, adapted, copied, translated, modified, edited or otherwise displayed or distributed in any manner without SGX's prior written consent. Please note that the general disclaimers and jurisdiction specific disclaimers found on SGX's website at http://www.sgx.com/wps/portal/sgxweb/footerLinks/tos#panelhead21 are also incorporated into and applicable to this document/material.