SGX: SGX Launches USD/INR (USD) Futures

SGX recently launched new USD/INR (USD) Futures on 23rd November 2020 to strengthen its ecosystem of Indian Rupee based derivative product offerings. This has been introduced as a complementary product to the market leading INR/USD FX Futures (IU) which alone constitute more than 60% of the global market share of offshore rupee based derivatives.

This will allow the participants including Asset managers, hedgers, arbitrageurs, CTAs and hedge funds to express a pure play directional view on the Indian currency.

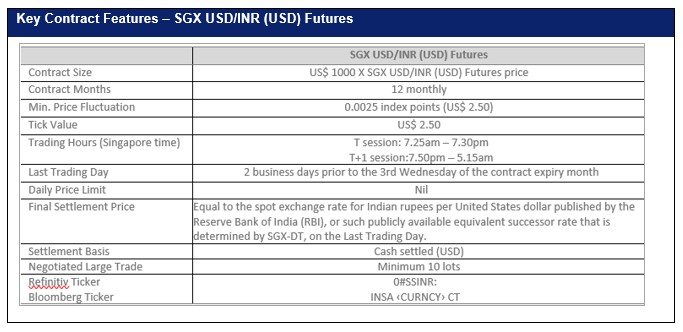

The new contract has monthly expiries aligned to the monthly IMM dates and the notional is denominated in US$ (contract specifications in the table below). SGX USD/INR (USD) Futures is the first FX contract at SGX to have a US$ notional and a US$ settlement. The notional multiplier is 1000 US$, so each contract offers a payoff equal to the 1000 x (Change in Contract Price) in US$ terms.

The new contract is structured as a “quanto” or an index contract so as to enable the price quotation conventions to be in line with the OTC markets. It also enables the participants to participate in the IMM Spreads market to express their view on the forward pricing of the FX curve. More information about the product can be found at https://www.sgx.com/derivatives/products/fx?cc=INR

Contract updates since Inception (23rd Nov – 11th Dec)

- A total of 10,939 lots were screen traded in the month of November since the launch date of 23rd November 2020 and another 12,332 lots have traded in the month of December (until 11th Dec)

- Majority of the trades came through in the T session (19,474 lots) and T+1 session saw 3,797 lots exchanging hands

- This translates to an inception to date DAV of approximately US$ 123 million or 1,662 lots

Example: Trade Price Convention

In the OTC USD/INR NDF market, prices are quoted in INR per USD, e.g. 74.5000. SGX USD/INR (USD) Futures (structured as a quanto) is quoted in a similar format, e.g. 74.5000 index points. So, if the participant is long 1 contract of INR, then for every point move in the contract price e.g. 74.5000 to 75.5000, he/she will make US$ 1000.