2020 and Livestock Markets - What Else Can Happen? by Tony Drake

Being a bit superstitious, I hesitated to write that headline after all that has occurred this year, but if there ever was a year that could be called a Black Swan trading event, I think we found it. A black swan event is defined as an extremely rare event with severe consequences that typically cannot be predicted beforehand. Between international trade disputes, COVID-19, plant interruptions, and volatile price action, the livestock producer has been through a lot this past year. We do not want to exclude the grain producer from an eventful year, as key Midwest grain producing states got hit with a derecho in early August - right near the end of the growing season - which some estimates say affected between 20 and 30 million acres in those states. It is best in years like this to take a full accounting of what has happened and try to figure out how to mitigate these events in the future. True, easier said than done. But if there is one key point I take away from this year, it is that agricultural producers/users need to understand and use risk management. I often hear about how volatile the price action was in the futures markets this year, but if the producer was hedged during events like we experienced this year, the numbers will prove that this added some financial cushion for the producing industry. We have seen this time and again when the markets get hit with outside influences - for example, the 2007/2008 economic crisis, trade disputes over the past few years, liquidations/expansions in livestock herds, and then of course throw in the COVID-19 impact.

But first, a bit of background is necessary on the livestock industry. As a country we typically do not produce enough beef for our needs and thus use the import markets to make up the gap. (We do export key premium cuts of beef to Asia, Mexico, and Canada, though.) In pork we have a slightly different picture where we export nearly 25% of our production, with a small but growing import market.

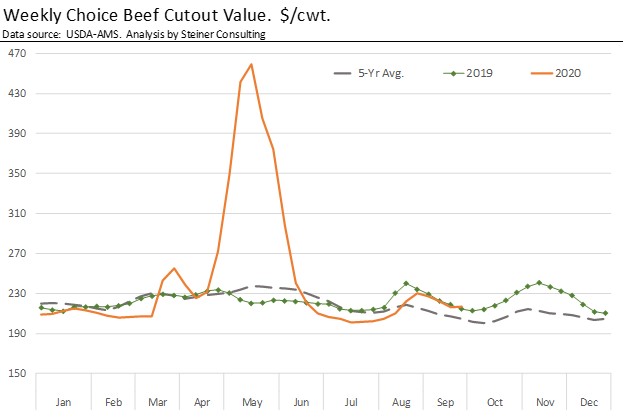

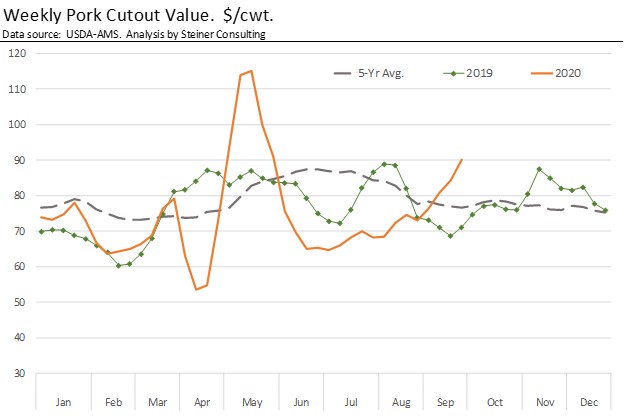

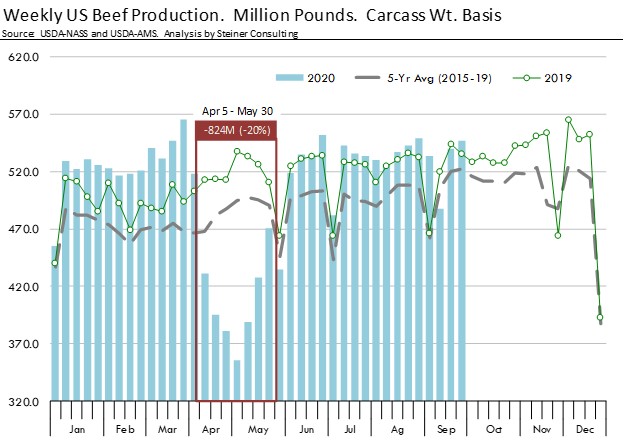

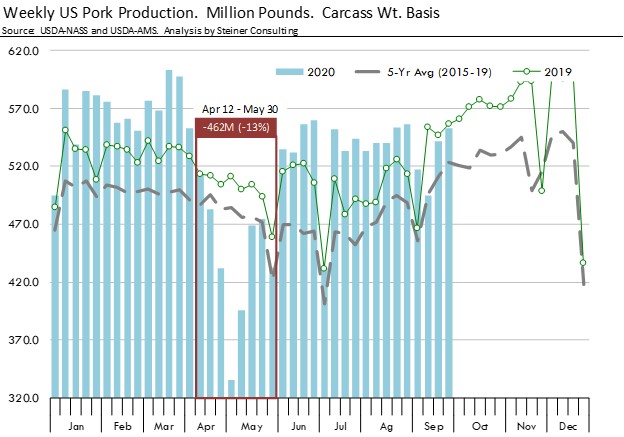

They say pictures are worth a thousand words, so I included a few charts around the livestock markets that will show just how extraordinary this year has been. Notice the huge swings in wholesale beef and pork prices. When the storylines hit earlier this year that there would be shortages of red meat at the grocery stores, a panic about hoarding ensued, but the media did not consider the whole picture - in particular, the drop in our beef and pork exports due to the higher domestic prices. At the same time, with restaurants and retail markets shutting down due to COVID-19, the market needed to change the flow from these key demand markets of restaurants to the grocery store. That change in logistics took time and effort by all in the trade, and this caused some price spikes for the consumer, but we did not have the shortage that our media wanted to talk about.

When COVID-19 began to infect the processing plant workers, this in turned slowed our production, thus the price spike at the retail level. This slower slaughter pace also put downward pressure on prices that the producer received for their cattle and hogs, since we could not get market-ready animals processed. I always compare the marketing of cattle and hogs to a ripe banana. There is typically a two-week marketing window for the animal, and if you miss that and the animal gets too large, the price that the producer will receive from the packer will be discounted. If you market too early, the animal will not be finished, and thus it will receive discounts on the quality. Looking forward, this backlogged livestock marketing issue will be what the industry will be working on for a few more months. On the demand side, our retail grocery store channels have slowly begun to return to nearly normal levels, but our restaurant trade will still be slow to recover, negatively affecting not only red meat demand but also the many jobs that restaurants support.

Circling back to the risk management thoughts from above, it is well documented that the livestock industry needs help around risk management. The recently released USDA investigative report on live cattle and boxed beef prices reaffirms this contention that the CME, brokers, and financial institutions need to put more resources around education for hedging. I surely do not have any easy answers for this education effort, but we must at least start this discussion. For example, looking back on 2020, the futures market gave something for both the short and long hedger this year in the way of basis movements. The short hedger benefited from a very positive basis (cash over futures) during the pandemic. Thus, the impacts of the lower cash cattle and hog prices that were so detrimental for the producer were lessened for short hedgers by this basis move. The large losses that our producers withstood this year truly did not have to happen if they were at least partially hedged. As for the long hedger, they are now finding better conversion with a slight negative basis (futures over cash) and a contango move with the back months expecting improvement in prices as we prepare for reduced cattle and hog numbers down the road. The futures markets are truly that, a market trying to determine what prices will look like in the future, and supply and demand play a vital role here.

Disclaimer: Trading in futures products entails significant risks of loss which must be understood prior to trading and may not be appropriate for all investors. Past performance of actual trades or strategies cited herein is not necessarily indicative of future performance. The information contained herein is provided to you for information only and believed to be drawn from reliable sources but cannot be guaranteed; Phillip Capital Inc. assumes no responsibility for errors or omissions. The views and opinions expressed in this letter are those of the author and do not reflect the views of Phillip Capital Inc. or its staff.