What a Trader Should Know About VIX Futures - Part 2

By CBOE

The CBOE Volatility Index, commonly known by its ticker VIX, is often referred to as the ‘fear index’. This moniker is a result of VIX often moving dramatically higher when the S&P 500 is under pressure. For example, when the US markets open and the S&P 500 is down 2% or 3% from the previous day’s close, the business media will quickly cite the day over day change for VIX which may be up 20% or 30% depending on market conditions.

In last month’s newsletter we mentioned the inverse relationship between the S&P 500 and VIX, but did not dive into why this relationship seems to exist. The table covers all trading days from the beginning of 1990 through August 2016.

|

Days SPX Up

|

Days SPX Up / VIX Down

|

% SPX Up / VIX Down

|

|

1739

|

1430

|

82.2%

|

|

Days SPX Down

|

Days SPX Down / VIX Up

|

%SPX Down / VIX Up

|

|

1448

|

1152

|

79.6%

|

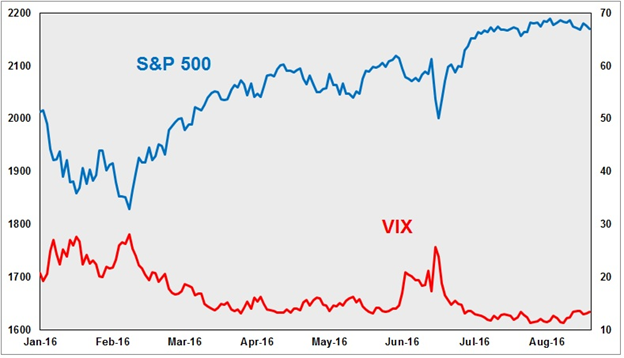

Note that about 80% of trading days the S&P 500 and VIX have moved in the opposite direction. This means that approximately one in five trading days both the S&P 500 and VIX will move in the same direction, but these days are typically low volatility days for the equity market. When the S&P 500 moves dramatically higher or lower the inverse relationship between the two is more evident. The chart below compares the daily price changes for the S&P 500 and VIX over the first eight months of 2016.

Note the rapid rise in VIX that occurred early in the year and then again in June. These are two instances of VIX quickly moving higher when the S&P 500 is under pressure. Also note that when the storm seems to have passed and the S&P 500 has resumed an uptrend that VIX reverts down to lower levels.

So a common question is, “Why the inverse relationship?” Or stated differently, “Why does VIX appear to only reaction to downside volatility?” This is the part of the relationship between the S&P 500 and VIX that is rooted in just how VIX is calculated.

The VIX Index calculation is determined using a wide variety of SPX option contracts. The calculation takes two different expiring series and uses the pricing of out of the money options to calculate VIX. When option prices rise, due to increased demand, the implied volatility of those options moves higher as well. You can think of VIX as a measure of increased demand for SPX options and that demand is often more aggressive for put options than call options.

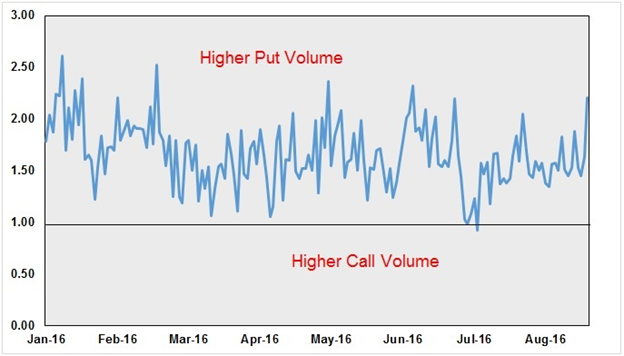

Also, more often than not, the volume for SPX put options is greater than the volume for SPX calls. The chart below shows the SPX put / call ratio for the first eight months of 2016. A put / call ratio is calculated by taking the put option volume and dividing that number by the call option volume on a certain day. If the ratio is over 1.00 we know that more puts than calls traded. Note for all but two trading days in 2016 there were more SPX puts than calls traded.

Both SPX call and put options are used to calculate VIX, but demand for puts may play a bigger role in day to day price changes for VIX. When traders are worried about the equity market, it is often when the market is trading lower. If the SPX is down 2% and a portfolio manager believes the market may trade even lower they may turn to SPX put options to provide downside protection. This activity will push option premiums higher and will also result in higher implied volatility as indicated by the pricing of those options. In the end this will result in VIX moving higher as well.

In the next issue we plan on discussing one of the best methods of gaining exposure to VIX, VIX futures contracts. VIX futures trading has grown tremendously since introduction in 2004 and average daily volume has been over 230,000 contracts with open interest recently setting records coming in well over 500,000. If you have further interest in market volatility CBOE will be hosting Risk Management Conferences (RMC) in Ireland (September 26 – 28) and Hong Kong (November 30 – December 1). More information about those conferences may be found at www.cboermc.com and finally for more information on VIX future check out www.cfe.cboe.com.

RISK DISCLAIMER: Trading in futures products entails significant risks of loss which must be understood prior to trading and may not be appropriate for all investors. Past performance of actual trades or strategies cited herein is not necessarily indicative of future performance. The information contained herein is provided to you for information only and believed to be drawn from reliable sources but cannot be guaranteed; Phillip Capital Inc. assumes no responsibility for errors or omissions. The views and opinions expressed in this letter are those of the author and do not reflect the views of Phillip Capital Inc. or its staff.