The Spot VSTOXX Index

by CFE

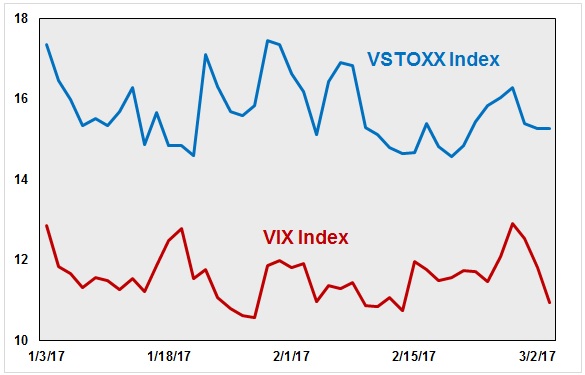

Behind VIX futures, the most actively traded futures contracts based on a volatility index are contracts based on the VSTOXX which is beast thought of as a European volatility benchmark. The spot VSTOXX index is calculated using option pricing from the Euro Stoxx 50 Index option market much like VIX is calculated from S&P 500 Index option prices. At times VSTOXX has been at a premium to VIX and there have been time periods where VIX has been higher than VSTOXX. Note in the chart below that for 2017, VSTOXX has maintained a pretty healthy premium to VIX.

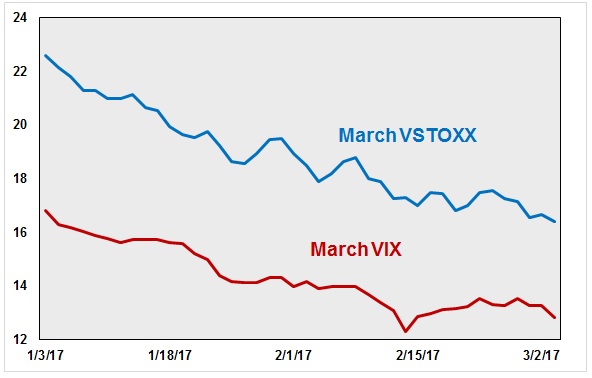

The futures contracts based on VSTOXX trade in a similar way to VIX futures in that they have an anticipatory pricing component. The chart below shows the daily pricing for the March VIX and March VSTOXX futures contracts. Note they tend to move in tandem with each other, but do have some small divergences.

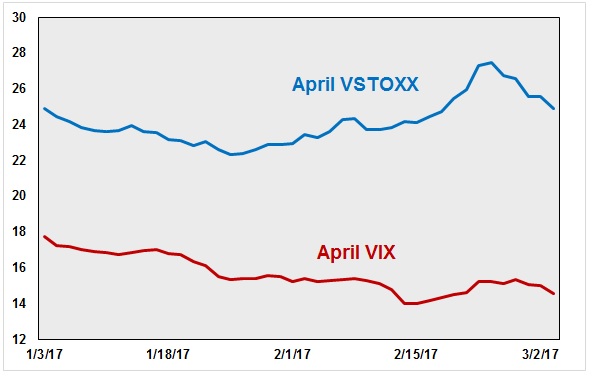

The volatility trading community has started to take note of the April VSTOXX futures pricing relative to spot VSTOXX as well as the April VIX futures contract. Although volatility indexes and associated futures are frequently influenced by current market price action, there are times where the markets take on an anticipatory component to the price action. With the pending French election process in April and May this appears to be happening with the VSTOXX futures. Note the chart below that shows the daily pricing for April VSTOXX and VIX futures and how there has been a consistent widening between the two markets.

With the introduction of extended hours trading for VIX futures there has been a steady rise in VIX – VSTOXX correlation trading where a trader may short one and buy the other based on an outlook for the spread between the two. The current price action in the April contracts may be offering an opportunity based on a trader’s outlook for the market reaction to next month’s election.

For example if a trader believes the VSTOXX futures are ‘too high’ relative to VIX and the risk associated with the election they may choose to short VSTOXX and buy VIX. Conversely, if they believe the European market is in for a period of downside volatility that is not fully reflected in the implied volatility of Euro Stoxx 50 options they may choose to buy VSTOXX and short VIX futures.

RISK DISCLAIMER: Trading in futures products entails significant risks of loss which must be understood prior to trading and may not be appropriate for all investors. Past performance of actual trades or strategies cited herein is not necessarily indicative of future performance. The information contained herein is provided to you for information only and believed to be drawn from reliable sources but cannot be guaranteed; Phillip Capital Inc. assumes no responsibility for errors or omissions. The views and opinions expressed in this letter are those of the author and do not reflect the views of Phillip Capital Inc. or its staff.