![]()

Back to Newsletter

Market Updates

Taiwan Begins 2017 on a Positive Note

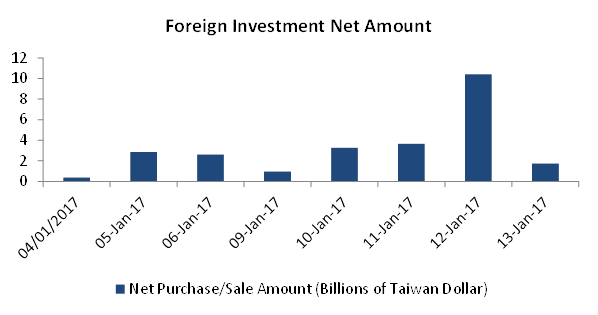

- Foreign institutional investors have become net buyers of Taiwan’s stocks for eight straight trading sessions since the start of the year - a reversal in trend of funds outflow which commenced since mid-December 2016.

- Taiwan stocks rose to their highest in more than 18 months, tracking gains in overseas markets. Gains were also boosted by Taiwan Semiconductor Manufacturing Co Ltd (TSMC), the world’s largest contract chipmaker, which climbed 1.4% ahead of its fourth-quarter results.

- SGX MSCI Taiwan Index Futures have seen a 25% increase in month-end open interest year-on-year. The open interest was 212,288 contracts, or approximately US$7.5 billion in notional value, as of 12 January 2017.

The Taiwanese equity market welcome the new year on a positive note. Foreign institutional investors have become net buyers of Taiwan’s stocks for eight straight trading sessions, a reversal in trend of funds outflow since mid-December 2016.

Net purchases from foreign institutional investors reached a high of NT$10.4 billion (US$329 million) as of 12 January 2017, according to the Taiwan Stock Exchange. The Industrials and Information Technology sectors outperformed, with YTD gains of 2% and 1.5% respectively, while the Energy and Healthcare sectors have underperformed.

Since the results of the US presidential elections, the MSCI Taiwan IndexSM has increased 4% to 351 index points, where among others, the Electronics sector outperformed, with YTD gains of 8.6%. In tandem, the TWSE index was up 0.8% at 9417 as of 12 January, rising to its highest since late June 2015. According to Sinopac’s research report, they foresee that two factors – strengthening exports and robust year-on-year corporate earnings – will lift the index to 9,500 to 10,000 index points in the first half of 2017.

Tapping Opportunities in the Emerging Markets Equities Space

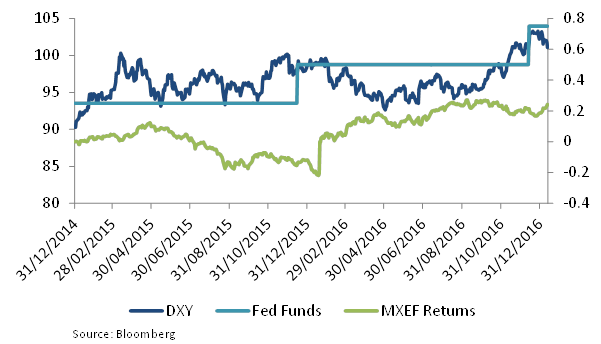

Emerging markets rallied and has outperformed the S&P Index up until mid-November 2016, where markets paused to react to the implications of a Trump presidency. Emerging market portfolios registered the lowest total inflows since 2008 as interest in developing economies waned. In December 2016, portfolio outflows totaled US$3.4 billion, resulting in 2016 having the weakest level of inflows for emerging markets since 2008., according to the Institute of International Finance (IIF).

Notwithstanding, the US President-elect has also promised more infrastructure spending and lower taxes. This, coupled with the December rate hike and impending rate hikes this year, the US dollar is expected to strengthen further, which may potentially lead to less attractive carry trades, outflows from emerging markets fixed income markets and weaker emerging markets currencies. The weaker emerging markets currencies might also in turn might boost exports of such economies which tend to be export-oriented in nature. This could present an interesting entry point for emerging markets equities as historically, emerging markets equities tend to outperform in times of strong US growth.

MSCI Emerging Markets (MXEF) Returns , US Federal Funds Rate (Fed Funds Rate), US Dollar Index (DXY)

SGX MSCI Taiwan Index Derivatives

One way to gain access into the emerging markets equities space is by investing in SGX MSCI Taiwan Index futures and options contracts. With 88 constituents, the MSCI TW IndexSM is a free-float adjusted market capitalisation weighted index designed to track the equity market performance of Taiwanese securities listed on the Taiwan Stock Exchange and GreTai Securities Market.

SGX MSCI Taiwan Index futures hit a high of 351 index points as of 12 January 2017, rising 4% since the results of the US presidential elections. The strengthening US dollar has further promoted the use of US dollar-denominated Quanto products such as SGX MSCI Taiwan Index futures and options. A Quanto product provides the returns of an underlying paid out in a hard currency such as the US dollar, without the currency translation, thereby offering direct exposure to equity risk premium.

SGX MSCI Taiwan Index Futures have seen a significant 25% year-on-year increase in month-end open interest. As of 12 January 2017, our open interest has reached 212,288 contracts, or approximately US$7.5 billion in notional value. The extended trading or T+1 session, which has been extended to 4:45am since 14 November 2016, allows market participants to take advantage of or hedge against price movements during European and US hours.

SGX MSCI Taiwan Index Futures Open Interest (Notional, in millions)

Contract Specifications

|

SGX MSCI Taiwan Index Futures |

|

|

Contract Size |

US$100 x SGX MSCI Taiwan Index Futures Price |

|

Ticker Symbol |

TW |

|

Contract Months |

2 nearest serial months and 12 nearest quarterly months |

|

Tick Value |

0.1 index point (US$10) |

|

Trading Hours (Singapore Time) |

T Session: 8:45am to 1:45pm T+1 Session: 2:15pm to 4:45am |

|

Last Trading Day (LTD) |

Second-last business day of the contract month |

|

Daily Price Limits |

(a) Whenever the Initial Price Limits are reached, i.e. the price moves by 10% in either direction from the previous day’s Daily Settlement Price (“DSP”), a Cooling Off Period is triggered where trading within the Initial Price Limits shall continue for a period of ten minutes. There shall be no price limits on the Last Trading Day for the expiring contract. With regards to the T+1 session, the Daily Settlement Price (DSP) derived in the T session that just ended will be the reference price to determine price limits. |

|

Position Limits |

A person shall not own or control more than 10,000 contracts net long or net short in all Contract Months combined, unless otherwise separately approved by the Exchange. |

|

Final Settlement Price |

The Final Settlement Price shall be the average of the MSCI Taiwan IndexSM values on the Last Trading Day taken at one-minute intervals during the last twenty-five (25) minutes of trading on the MSCI Taiwan IndexSM preceding the commencement of the closing auction session, and the closing index value. The Final Settlement Price shall be rounded to two decimal places. |

|

Settlement Basis |

Cash settled (USD) |

|

Margins Offset |

Yes |

|

Negotiated Large Trade |

Minimum 50 lots |

|

Price Information (Vendor: Ticker) |

Thomson Reuters: STW: <F3> Bloomberg: TWA <INDEX> CT |

|

SGX MSCI Taiwan Index Options |

|

|

Contract Size |

One SGX MSCI Taiwan Futures contract |

|

Contract Months |

2 nearest serial months and 12 quarterly months |

|

Tick Value |

0.01 index point (US$1.00) |

|

Trading Hours (Singapore Time) |

T Session: 8:45am to 1:50pm T+1 Session : 2:15pm to 4:45am |

|

Last Trading Day (LTD) |

Second-last business day of the contract month |

|

Strike Prices |

Five index point intervals

|

|

Position Limits |

A person shall not own or control options and underlying MSCI Taiwan Index Futures contracts that exceed 10,000 futures-equivalent contracts net on the same side of the market in all contract months combined. Note: Clearing Members may apply to the Exchange for higher position limits on behalf of their customers. Approval is based on the financial standing of the Member and their customer on a case by case basis. |

|

Option Exercise |

European Style |

|

Settlement Basis |

Cash settled (USD) |

|

Margins Offset |

Yes |

|

Negotiated Large Trade |

Minimum 25 lots |

|

Price Information (Vendor: Ticker) |

Thomson Reuters: STWs: <F3> Bloomberg: TWA <INDEX> OMON |

My Gateway

SGX’s investor education portal with market, product and investment information and events. Sign up now at sgx.com/mygateway to receive our investment updates and economic calendar.

SGX StockFacts

Whether you are seeking new or established companies to invest in, SGX StockFacts can provide you with the information you need to identify and understand the stocks that best fit your investment strategy. Visit now at sgx.com/stockfacts.

This document is not intended for distribution to, or for use by or to be acted on by any person or entity located in any jurisdiction where such distribution, use or action would be contrary to applicable laws or regulations or would subject SGX to any registration or licensing requirement. This document is not an offer or solicitation to buy or sell, nor financial advice or recommendation for any investment product. This document has been published for general circulation only. It does not address the specific investment objectives, financial situation or particular needs of any person. Advice should be sought from a financial adviser regarding the suitability of any investment product before investing or adopting any investment strategies. Investment products are subject to significant investment risks, including the possible loss of the principal amount invested. Past performance of investment products is not indicative of their future performance. While SGX and its affiliates have taken reasonable care to ensure the accuracy and completeness of the information provided, they will not be liable for any loss or damage of any kind (whether direct, indirect or consequential losses or other economic loss of any kind) suffered due to any omission, error, inaccuracy, incompleteness, or otherwise, any reliance on such information. Neither SGX nor any of its affiliates shall be liable for the content of information provided by third parties. SGX and its affiliates may deal in investment products in the usual course of their business, and may be on the opposite side of any trades. SGX is an exempt financial adviser under the Financial Advisers Act (Cap. 110) of Singapore. The information in this document is subject to change without notice.