What Volatility Approaches Have Worked in 2017?

By Cboe

2017 is set to go down as the least volatile year in decades for the US equities markets. One month realized volatility for the S&P 500 has been in the single digits, at times even low single digits, for all of this year. VIX, which is a measure of the market’s expectations for volatility, should finish 2017 with an all-time low when looking at the average closing price in 2017. The chart below shows the high, low, and average for VIX by year going back to 1990.

So what has been working in 2017? Of course owning stocks has been an effective strategy, but what has worked in the volatility space? Cboe has a method of demonstrating this through a suite of performance indexes broken down into different volatility market approaches. These four indexes along with their performance for the first nine months of 2017 appear on the table below.

|

Cboe Eurekahedge Short Volatility Index |

12.95% |

|

Cboe Eurekahedge Long Volatility Index |

-11.50% |

|

Cboe Eurekahedge Relative Value Volatility Index |

9.88% |

|

Cboe Eurekahedge Tail Risk Index |

-20.10% |

The names of each of these indexes is fairly self-descriptive, but for clarity sake here is a quick rundown of each index. The short volatility index measures the performance of hedge funds who take a net short view on implied volatility and the long volatility index provides a measure of the performance of hedge funds who take a net long view on implied volatility. The relative value index tracks the performance of hedge funds who trade relative value of opportunistic volatility strategies. Finally, the tail hedge index provides a broad measure of performance of hedge funds that specifically seek to achieve capital appreciation during times of extreme market stress.

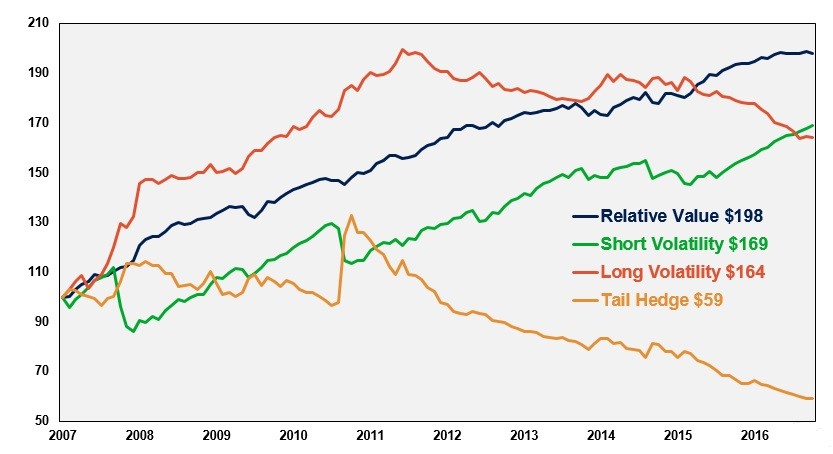

Performance wise, the short volatility and relative value volatility indexes have had a good year, while being long volatility and using volatility to hedge against a large drop in the US stock market have both done poorly. Over the long-term each of these four strategies has had their day in the sun, even the tail hedge index. The chart below shows the result of $100 being invested in each of the Cboe Eurekahedge indexes on the last day of 2007 through the end of September 2017.

Long volatility worked well from 2007 through 2011, but has fallen off due to low stock market volatility which has resulted in a low VIX. The tail hedge index had quite a return in 2008 and again in 2011 benefitting from stock market weakness that translated into higher volatility expectations as indicated by VIX. Over the long term short volatility hit a couple of speed bumps, but the performance line is a good example of the pattern of returns that would be expected from a short volatility strategy. Finally, the relative value index has been a consistent performer as the funds in this area take advantage of volatility spikes as well as differences in volatility levels among markets.

The low volatility market that has been 2017 has been good to short volatility players as well as the relative value funds. This is a prime example of how well short volatility strategies works in a low volatility environment.

RISK DISCLAIMER: Trading in futures products entails significant risks of loss which must be understood prior to trading and may not be appropriate for all investors. Past performance of actual trades or strategies cited herein is not necessarily indicative of future performance. The information contained herein is provided to you for information only and believed to be drawn from reliable sources but cannot be guaranteed; Phillip Capital Inc. assumes no responsibility for errors or omissions. The views and opinions expressed in this letter are those of the author and do not reflect the views of Phillip Capital Inc. or its staff.