![]()

BAck to Newsletter

Asymmetric Returns: Nikkei 225 Index Outperforms TOPIX Index

09/28/16

By SGX

- Japanese benchmark Nikkei 225 Index diverges from the TOPIX Index as the Nikkei-TOPIX ratio achieves the highest level since 1999 on the back of central bank ETF purchases.

- The Bank of Japan stimulus programme favours the Nikkei 225 Index since more than half of eligible ETF assets under management are marked to the Nikkei 225 Index.

- According to the Reuters Corporate Survey, Japanese corporates are “disappointed” with the fiscal stimulus unveiled by Prime Minister Abe, while market expectations for more stimulus measures resulting from the Bank of Japan September meeting have increased.

Nikkei 225 Index Breaks Away From TOPIX Index

Divergence between the two major Japanese equities benchmarks, the Nikkei 225 Index and the TOPIX Index, accelerated over the past month following the central bank policy meeting at the end of July. On 29 July, the Bank of Japan (BOJ) effectively doubled its firepower when it increased its annual ETF buying target from 3.3 trillion yen (US$33 billion) to 6 trillion yen (US$60 billion).

The BOJ specifies that its ETF purchases are limited to those tracking certain Japanese equity indices, namely the Nikkei 225 Index, the TOPIX Index, and the JPX-Nikkei 400 Index. The Nikkei 225 Index has turned out to be the largest beneficiary from the BOJ ETF programme due to the relatively large assets under management (AUM) of the Nikkei 225 Index ETFs.

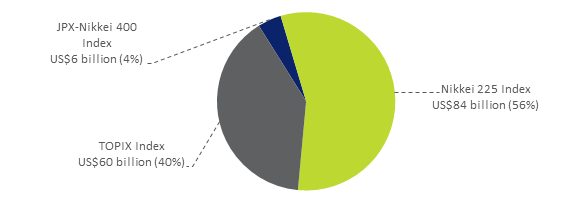

Figure 1: Assets Under Management of BOJ-Eligible ETFs by Underlying Index

Source: Bloomberg, 23 August 2016

Domestically-listed ETFs based on the Nikkei 225 Index account for approximately 56% of the ETF universe eligible for the central bank purchase programme. Since the BOJ specifies that “the Bank's purchase would roughly be proportionate to the total market value of that ETF issued”, the largest proportion of the BOJ’s ETF purchases are those that track the Nikkei 225 Index. CLSA‘s Nicholas Smith estimates that 55% of ETF purchases are the Nikkei 225 stocks versus only 41% for the TOPIX.

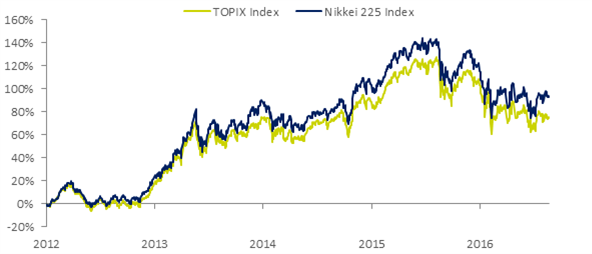

The central bank’s ETF purchase programme has resulted in market asymmetries, most obvious of which is the outperformance of the Nikkei 225 Index over the TOPIX Index. Last week, the Nikkei-TOPIX ratio (NT Ratio), a measure derived by dividing the index level of the Nikkei 225 Index by the index level of the TOPIX Index, achieved the highest level in 17 years of 12.8.

Figure 2: Performance of Nikkei 225 Index and TOPIX Index (Base = 4 Jan 2012)

Source: Bloomberg, 23 August 2016

Figure 3: NT Ratio = Nikkei 225 Index / TOPIX Index

Source: Bloomberg, 23 August 2016

PM Abe “Disappoints” With Latest Stimulus

Earlier this month, Prime Minister Abe announced 4.6 trillion yen (US$45 billion) in new government spending this fiscal year in a bid to shore up the economy and overcome deflation. The package includes US$24.5 billion in welfare spending, while 22 million low income individuals will receive US$147 each.

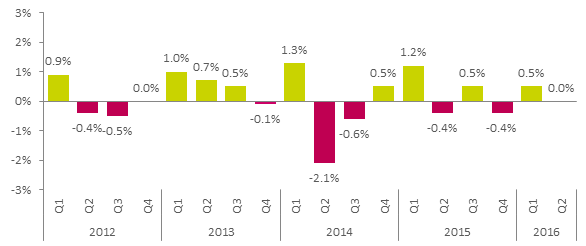

Japanese companies were reportedly underwhelmed by the stimulus announcement and believe there will be little economic impact, according to the Reuters Corporate Survey conducted from 1 to 16 August 2016. Market sentiment remained poor over the month with last week’s worse-than-expected second quarter GDP figures. On a quarter-on-quarter basis, the economy showed no growth versus economist expectations of a 0.2% rise.

Figure 4: Japan Quarter-on-Quarter GDP (%)

Source: Bloomberg, 23 August 2016

Market expectations for more stimulus at the upcoming 20 and 21 September BOJ policy meeting have grown. According to an interview published by Japan’s Sankei newspaper, BOJ Governor Kuroda said results of a comprehensive policy review will be published and that there is “sufficient chance” the central bank will add to its easing in the September meeting.

Access Japan's Volatility and Liquidity With SGX Nikkei Derivatives

SGX offers a comprehensive suite of Japan-related equity derivatives to cater to the needs of investors, including the Yen Nikkei 225 Index Futures and Options, USD Nikkei 225 Index Futures, and the Nikkei Dividend Futures.

SGX offers extended trading hours for the Nikkei 225 Index Futures and Option from thirty minutes ahead of the Japan stock market opening at 7.30 am Singapore Time, up until 2am Singapore time, covering the London close.

In addition, SGX’s Japan-related equity derivatives remain available for trading on all Japan holidays, with the exception of New Year’s Day (1 January). Margin discounts on spreads formed with other SGX derivatives allow for greater capital efficiency for investors that has views on multiple Asian markets.

Cross-Product Margin Offsets

|

Contract |

Contract |

Margin Offset |

|

SGX USD Nikkei 225 Index Futures |

SGX Nikkei 225 Index Futures |

93% |

|

SGX MSCI China Index Futures |

SGX Nikkei 225 Index Futures |

40% |

|

SGX MSCI Taiwan Index Futures |

SGX Nikkei 225 Index Futures |

40% |

|

SGX Nifty 50 Index Futures |

SGX Nikkei 225 Index Futures |

40% |

|

SGX MSCI Singapore index Futures |

SGX Nikkei 225 Index Futures |

40% |

|

SGX FTSE China A50 Index Futures |

SGX Nikkei 225 Index Futures |

35% |

|

SGX Nikkei Dividend Index Futures |

SGX Nikkei 225 Index Futures |

15% |

Source: SGX (data as of 23 August 2016)

For more information, please visit www.sgx.com/derivatives/nikkei225.

My Gateway

SGX’s investor education portal with market, product and investment information and events. Sign up now at sgx.com/mygateway to receive our investment updates and economic calendar.

SGX StockFacts

Whether you are seeking new or established companies to invest in, SGX StockFacts can provide you with the information you need to identify and understand the stocks that best fit your investment strategy. Visit now at sgx.com/stockfacts.

This document is not intended for distribution to, or for use by or to be acted on by any person or entity located in any jurisdiction where such distribution, use or action would be contrary to applicable laws or regulations or would subject SGX to any registration or licensing requirement. This document is not an offer or solicitation to buy or sell, nor financial advice or recommendation for any investment product. This document has been published for general circulation only. It does not address the specific investment objectives, financial situation or particular needs of any person. Advice should be sought from a financial adviser regarding the suitability of any investment product before investing or adopting any investment strategies. Investment products are subject to significant investment risks, including the possible loss of the principal amount invested. Past performance of investment products is not indicative of their future performance. While SGX and its affiliates have taken reasonable care to ensure the accuracy and completeness of the information provided, they will not be liable for any loss or damage of any kind (whether direct, indirect or consequential losses or other economic loss of any kind) suffered due to any omission, error, inaccuracy, incompleteness, or otherwise, any reliance on such information. Neither SGX nor any of its affiliates shall be liable for the content of information provided by third parties. SGX and its affiliates may deal in investment products in the usual course of their business, and may be on the opposite side of any trades. SGX is an exempt financial adviser under the Financial Advisers Act (Cap. 110) of Singapore. The information in this document is subject to change without notice.

RISK DISCLAIMER: Trading in futures products entails significant risks of loss which must be understood prior to trading and may not be appropriate for all investors. Past performance of actual trades or strategies cited herein is not necessarily indicative of future performance. The information contained herein is provided to you for information only and believed to be drawn from reliable sources but cannot be guaranteed; Phillip Capital Inc. assumes no responsibility for errors or omissions. The views and opinions expressed in this letter are those of the author and do not reflect the views of Phillip Capital Inc. or its staff.